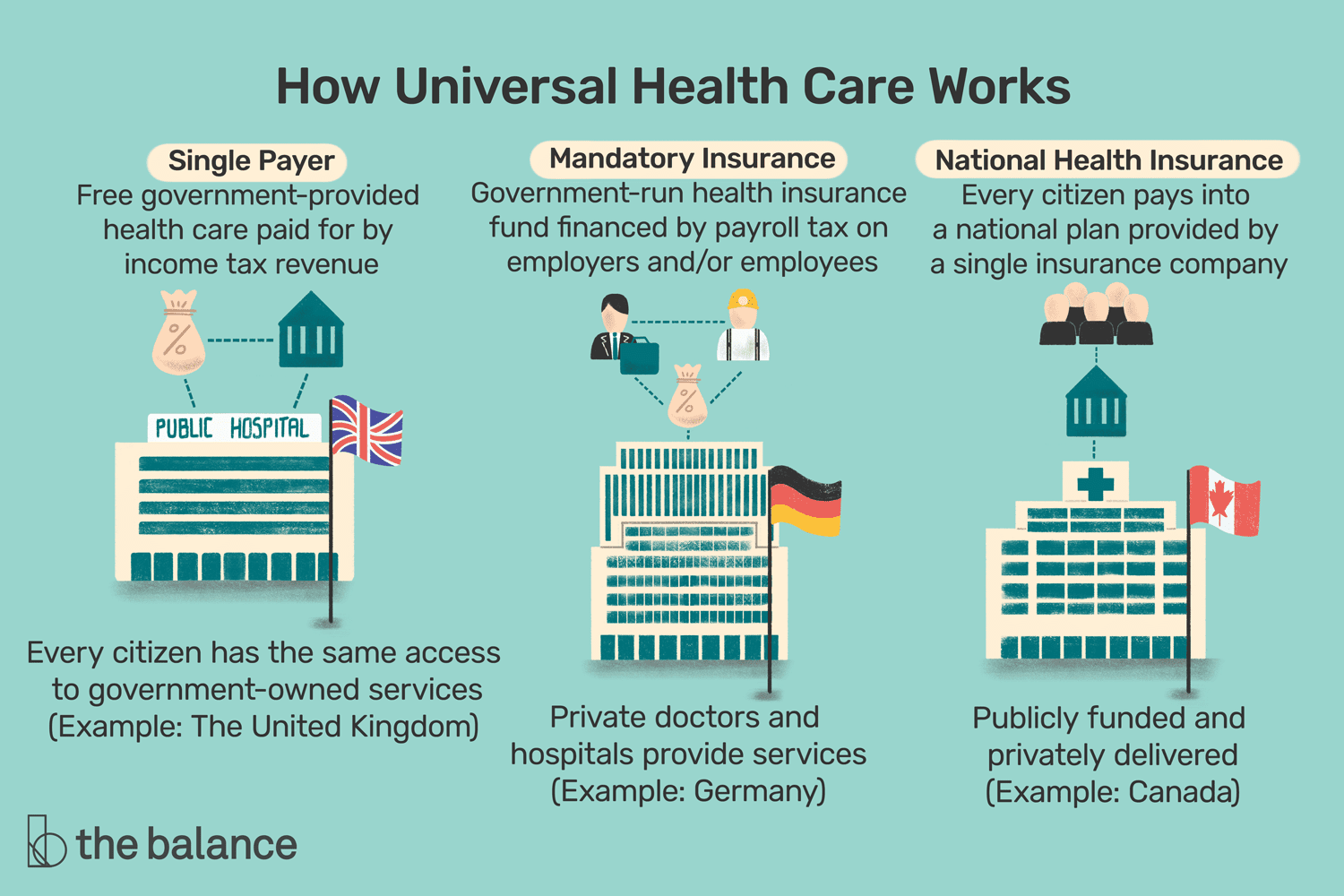

Universal Healthcare Saves Money And Solves Problems.

Single-Payer Healthcare For All Would Cost Less, Help More, And Erase Paperwork.

With Donald Trump levying the largest Medicaid cuts in American history in his “One Big Beautiful Bill”, which also includes $500 billion in medicare cuts, healthcare finds itself back on the forefront.

Which raises a prescient question, why does America still refuse to guarantee all its people access to health insurance?

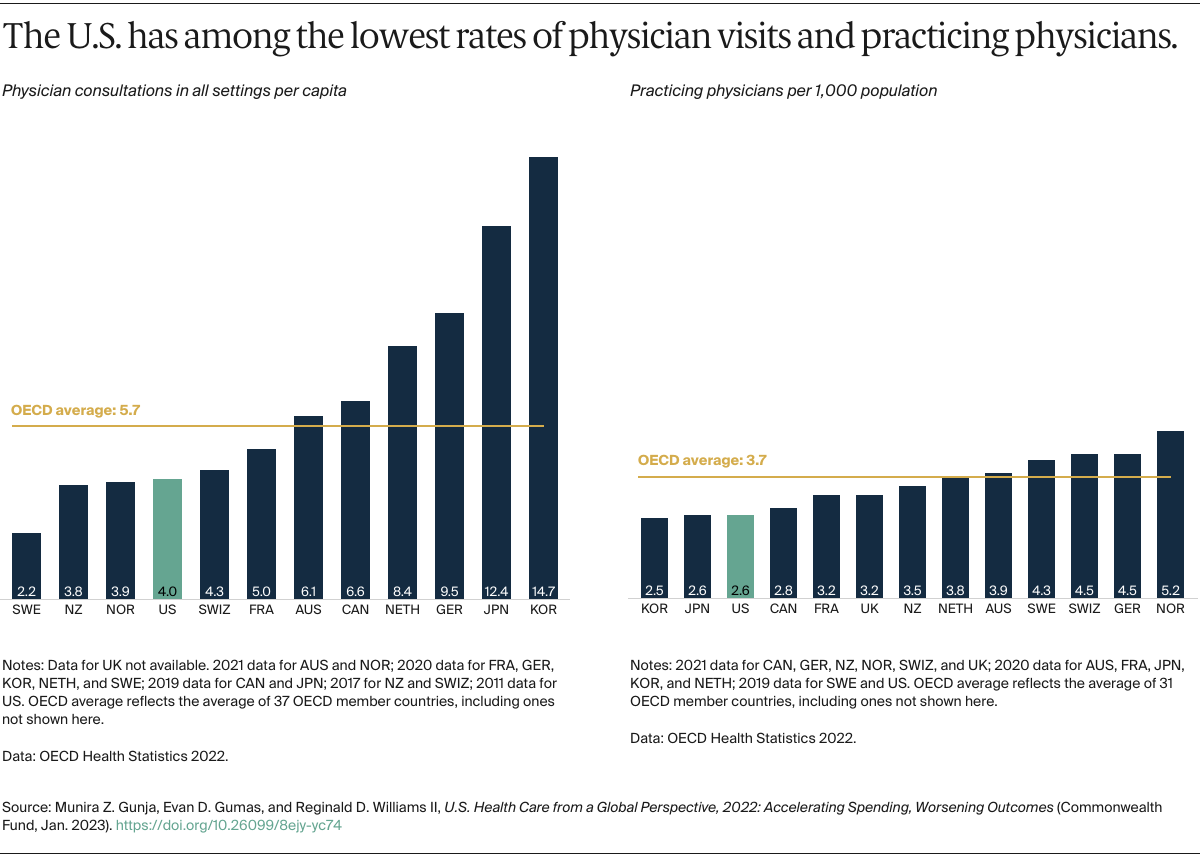

It’s not for success of our current model. America currently spends the most on health expenditures per capita of any country, yet 91 million Americans cannot access quality healthcare if needed.

Roughly another 26 million Americans are completely uninsured and would be left with crippling debt if they needed to visit a hospital.

It begs the question, where is this money going?

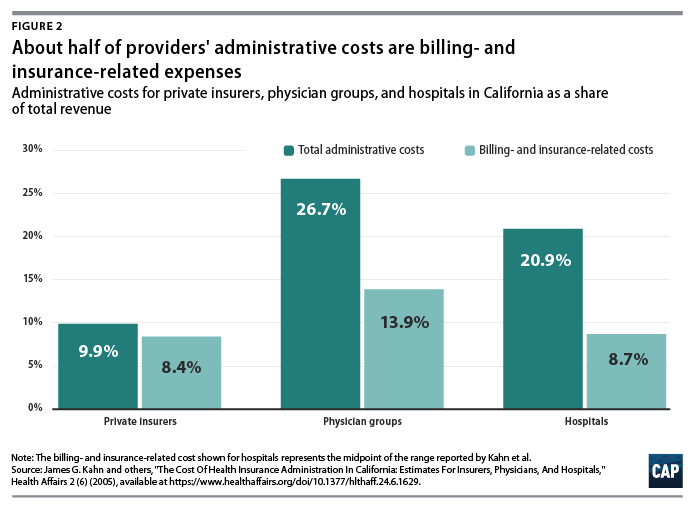

The best answer is administrative costs and profits. Right now, healthcare providers in the United States spend roughly $496 billion on billing and insurance-related costs, according to Center for American Progress estimates.

These are costs not directly pertaining to medical practices, like marketing, processing, overhead, and more.

The National Academy of Medicine estimated in a report this is upwards of double the necessary amount for our healthcare system, with that excess alone reflecting $248 billion each year.

A 2010 analysis between the US system and Canada found the largest share in difference of spending, 38%, was administrative costs. Because of this administrative burden, we have over 40% more administrative staff and spend 50% more time on administrative tasks than Canada.

While these administrative costs are burdensome for private insurers, public insurers like Medicare see this cost lower than 2%, or $9 billion of nearly $700 billion in Medicare’s case. This is also true with single-payer universal systems in other countries compared to America.

Additionally, and largely in-part due to these administrative burdens, private insurance spending grows at a faster rate than public insurance. For instance, a private insurance plan equal to medicare would cost 40 times the price on average.

The other place the spending is going is directly into the pockets of wealthy CEOs.

Insurance works by pooling together the money everyone pays into it, private insurance then figures they need a set percent of that money to reach their bottom line in profit.

The left over funds are given out on an “as-needed” basis, where the need is determined by the insurer, not the customer. This leads to services being denied strictly for profit-based reasons, even when it could be life saving.

This is counterproductive for the customer for a multitude of reasons, your “pool” of money is always limited by the amount of people with the same insurance. The more private insurances, the more tiny pools rather than one big one.

It is then once again limited by the amount of profit the corporation expects to receive each year. If your insurance pool is already limited to 2% of the population and the insurer takes 50% of what that population pays in, you can see how your piece of the pie only gets smaller and smaller.

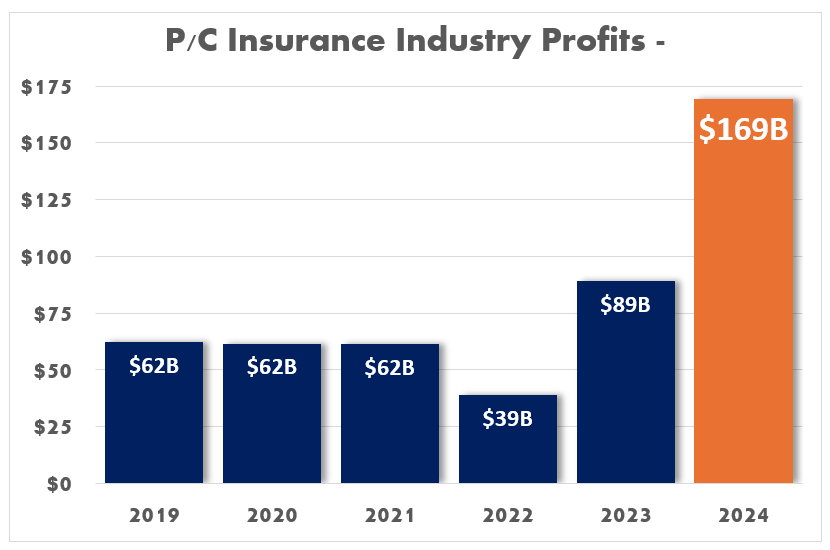

It’s not like these private insurers are barely scraping by, they made record profits in 2024 to the tune of almost $170 billion. In the last decade, health insurance profits have skyrocketed over 230%.

Hospital and clinical services make up over one-third of healthcare expenditures in America largely due to fees charged to private insurers being inconsistent with the quality of services.

The average cost of giving birth in Spain is $2333 compared to $14,910 in America, yet the rate of neonatal mortality in the US is double what we see in Spain. Furthermore, appendectomy fees in the US can vary from $9,332 to $33,250, with an inverse correlation to the outcomes of these services.

Just through applying Medicare in a “for all” system that everyone pays taxes into and receives would see hospital fees reduced by 5.54% and clinical services by 7.38%, totaling a yearly discount of $100 billion.

This represents $768 billion in additional burden for providers. Estimates find that consolidation of billing into a unified system can reduce this expenditure by $284 billion, more than double the proposed change in fees.

Another unspoken of issue in our current system is the fact that overwhelming paperwork is a primary factor in physician burnout. Through elimination of unpaid bills, this workload would be drastically reduced in a universal healthcare model.

When considering the costs of coverage expansion in a universal healthcare model, as well as savings that would be achieved through elimination of administrative tasks, medicine price negotiations, and the elimination of a profit motive, it’s calculated that a single-payer, universal healthcare system is likely to lead to a 13% savings in national healthcare expenditure, or over $450 billion annually.

Additionally, estimates find that ensuring healthcare access for all Americans would save over 68,000 lives and 1.73 million life-years every year.

The case for universal healthcare is a logical, moral, and economic no-brainer. It saves money and saves lives, while making doctors jobs easier.

It’s time for universal healthcare in America.